Table of Contents

Download Planning for a New Northeast Corridor:

Download The Hudson Terminal Plan:

Download the Trends & Opportunities Report:

Other Methods of Capturing Value

There are a number of other ways in which government agencies charged with developing TODs are able to capture the added value created by new transportation infrastructure projects. One of the most common strategies is through the assessment of district-specific taxes on properties directly benefiting from a transportation infrastructure project, which operate similarly to PILOT agreements. One recent example of the utilization of special district assessment taxes was the construction of the Washington Metro’s NoMa – Gallaudet U Station in 2004. As part of the project’s financing, private landowners set to benefit from the station’s construction agreed to pay a special assessment tax over 30 years to raise $25 million of the $100 million total project cost. This special assessment tax will be charged on top of regular property taxes for nonresidential parcels located within 2,500 feet of the future station’s entrances. The Washington Metropolitan Area Transit Authority financed the project, in part, by issuing bonds that will be repaid using the funds collected through the special assessment tax over the subsequent decades.

Denver Union Station Redevelopment Rendering

Another method of capturing value from TODs is through Tax Increment Financing (“TIF”), which involves promising future tax revenues to secure present financing arrangements. Since infrastructure improvements increase property values, which results in higher tax revenues, government agencies are able to leverage those future revenues through TIF proposals in order to finance a given infrastructure project. For example, as part of its $488 million redevelopment of Denver Union Station, the Denver Union Station Project Authority (“DUSPA”) obtained a $155 million, 3.91%, 30-year loan from the Federal Railroad Administration’s Railroad Rehabilitation and Improvement Financing (“RRIF”) program, which operates similarly to the US DOT’s TIFIA program. In order to secure and pay for the RRIF loan, the Denver Downtown Development Authority, which oversees TOD within the 40-acre project site, agreed to appropriate all tax increment revenue over the next 30 years to DUSPA. Because TIF relies on predicting future tax revenue, the City and County of Denver agreed to appropriate up to $8 million annually during the term of the RRIF loan to cover any potential shortfalls in tax increment revenues.

Another popular method of capturing added value is through public-private joint ventures. Since transit agencies often lack the expertise and resources to develop certain aspects of TODs on their own, they may enter into joint development agreements with private partners to construct TODs on publicly-owned land. For the HYRP, this involved the leasing of the publicly-owned Eastern Rail Yard to a joint venture between the Related Companies and Oxford Properties. In another example, funding for a the 2011 construction of the West Dublin/Pleasanton infill commuter station outside of San Francisco was achieved through a public-private partnership between Bay Area Rapid Transit (“BART”) and private developers. Under the arrangement, the private developers prepaid $15 million of the $100 million project cost for a ground-lease to develop a transit village on three acres of government-owned land adjacent to the new station. In addition to the one-time payment, the developers also agreed to pay BART a fee for every sale of residential units within the development, which would allow BART to continue to capture value from its new station.

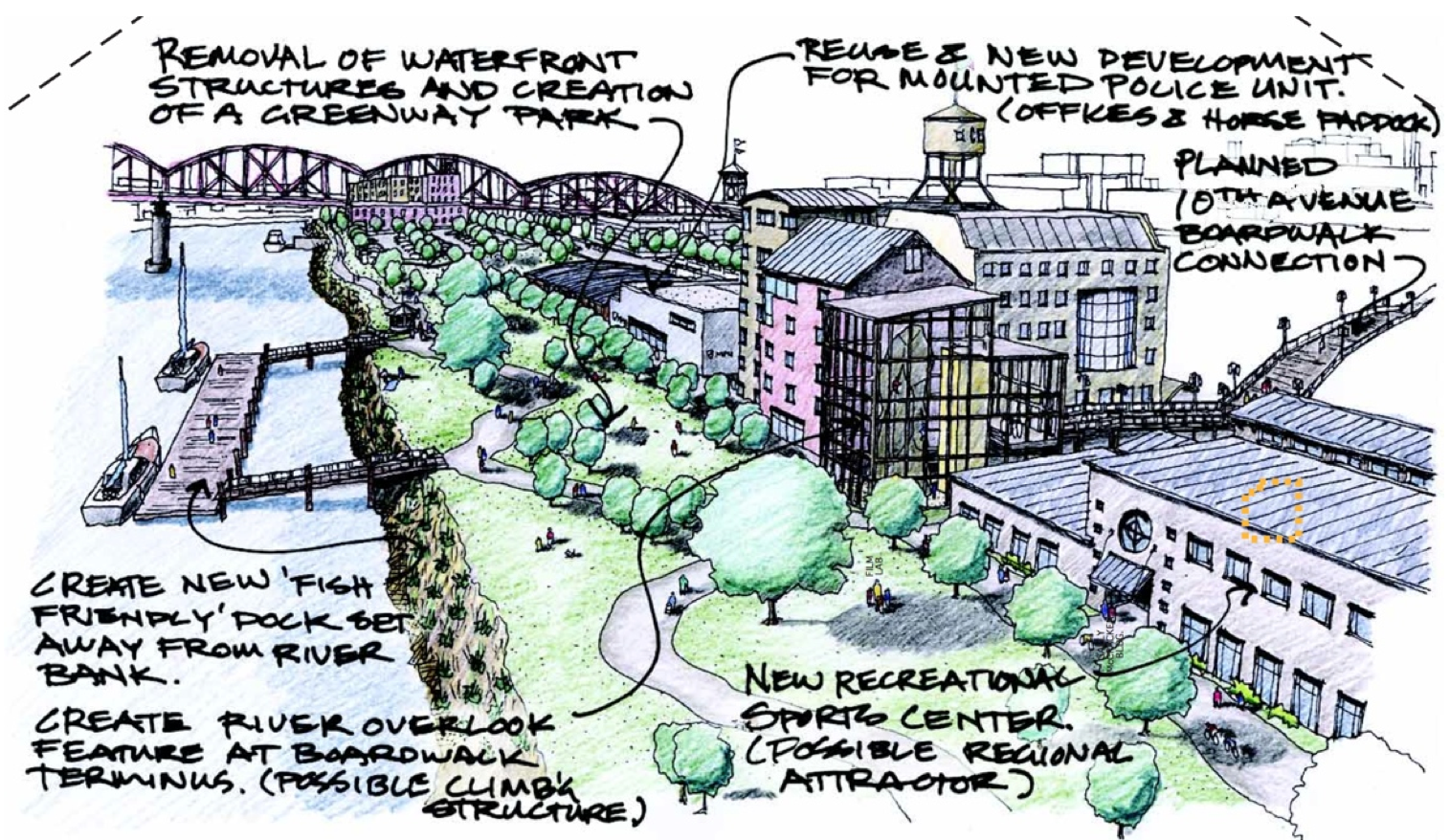

Portland’s Pearl District Development Plan Rendering (2001)

Public-private partnerships may also be used in instances where the sale or lease of public land is not available. Private investment can be leveraged where public entities engage in risk-mitigation of private developments through environmental remediation, entitlement and construction risk mitigation, financing assistance, and marketing of a given TOD. In Dallas, for instance, the Dallas Area Rapid Transit Authority (“DART”) engages developers by providing market analyses for transit projects, which in turn reduces predevelopment costs. In another example from the late 1990s, the City of Portland negotiated with the owner of a 40-acre parcel of land adjacent to the proposed alignment of a new streetcar extension to increase the minimum construction density of residential and commercial development within the project site in exchange for bringing the streetcar past the owner’s property and making other area improvements. Almost 20-years later, the neighborhood of the TOD is today one of the most popular areas in the city and, at build-out, will be home to 10,000 residents and over 20,000 jobs. The success of this public-private partnership has led to the expansion of the streetcar system in Portland and creation of new, more extensive joint TOD ventures.